They go by various names: ‘overdrawn shareholder current account’, ‘shareholder loan’, but it’s the same thing, you borrowed some money from your own company, and now the government wants you to pay it back, or pay the taxes.

For many, the first word of the crackdown came with Nicola Willis’ Budget on 28 May. But it was telegraphed last year, and, as announced, it is markedly more lenient than what IRD originally recommended.

What was announced

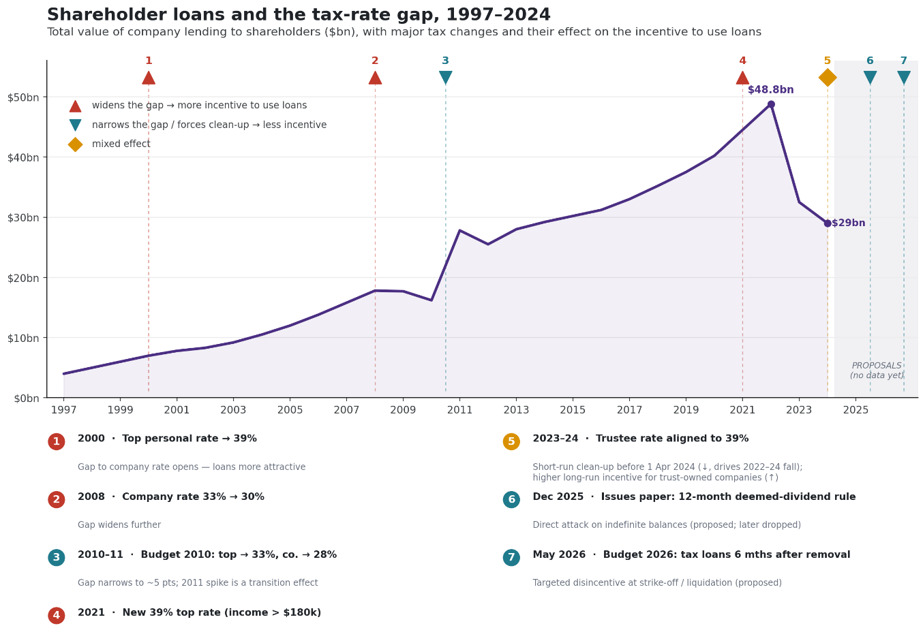

The proposed measure is straightforward: where a company is removed from the Companies Register that is still owed money by its shareholder, that balance becomes the shareholder’s taxable income six months after removal. Treasury and Inland Revenue put the yield at about $146 million over the 2026 to 2030 forecast period. To give you a completely useless sense of scale, that’s enough money to fund the Ministry for Women for 10 years!

It is a pared-back version of a far broader December 2025 proposal that would have deemed many new shareholder loans above a de minimis threshold to be dividends if not repaid within 12 months after the end of the income year in which they were made.

But instead of a turgid piece about the proposed policy, and the now revised plan, I wanted to understand how we got here. Why do Kiwi’s love borrowing money from their own companies.

Show me the incentive and I’ll show you the outcome

So why do these balances exist at such scale; $29 billion across 119,000 companies in 2024, on Inland Revenue’s figures, around 3.5 times those companies’ taxable income? Begin with tax. Distribute a profit as a dividend and the shareholder tops up from the 28% company rate to their own, that’s eleven points for a 39% earner. Lend it instead, charge the prescribed interest rate, and there is no immediate top-up.

The incentive tracks the gap between the company rate and the top personal and trustee rates, and our tax history has repeatedly widened it: the 39% top rate arrived in 2000, the company rate fell to 28% by 2011, the 39% rate returned in 2021, and the trustee rate followed in 2024. Inland Revenue’s own data shows shareholder loans growing about 8.7% a year since 1997 and peaking at $48.8 billion in 2021–22, the first full year of the restored 39% rate, and the IRD concedes the trend “appears to reflect changes in personal tax rates.” Note what the Budget measure does not do: it leaves that gap untouched.

But tax isn’t the whole story

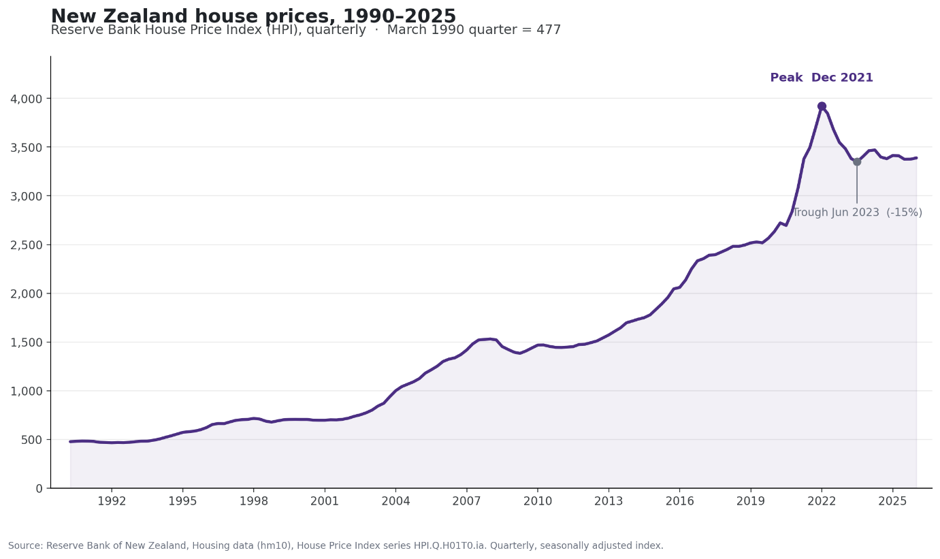

It is lazy, though, to blame tax alone. More likely, the loan story is also an economic environment story, and in New Zealand that has long meant the housing market.

Treat the closely held company as a private bank with a single customer. A wonderful one, if you are the customer: it lends at the prescribed rate (as low as 4.50% through 2020–22), asks no questions, sets no loan-to-value ratio, runs no serviceability test, demands no repayments, and lets the interest capitalise quietly onto the balance. Point that at an asset rising tax free, faster than the cost of carrying it. Draining the company to buy property was a rational decision. The 2022 peak was not just the 39% rate, it was low interest rates and a national belief that residential property always goes up, and delivers a tax free capital gains bonanza.

And why the line is now falling

What stacks, unstacks. Prices fell about 15% to a trough in May 2023 and remain a fifth to a quarter down in Auckland and Wellington. The prescribed rate roughly doubled to 8.41% by late 2023, rental interest deductibility was (temporarily) stripped away, and the dream evaporated. And a private bank can only lend if it is making money, the real estate and construction firms that dominate this book aren’t, so origination has dried up. The fall to $29 billion by 2024 is, I suspect, both blades of the scissors, solvent owners clearing balances with dividends and salaries, and distressed ones whose loans are now stuck, bound for a liquidator.

Where this leaves us

The irony is that the measure arrives to discipline a behaviour already in retreat, which is why even its modest revenue estimate may prove optimistic. The simplest way to avoid a tax triggered by removal is, after all, to keep these entities registered and never pay the tax. These changes do nothing to remove the incentives that created the problem in the first place, and if our property market dream is ever rekindled, we will start borrowing again. When profits and property recover, as they always seem to in this country, the incentive will be waiting.